Here is our house view on the recent volatility in the local and global stock markets. Information and data was sourced from Morningstar, Commsec, Yahoo!7 Finance, Fat Prophets newsletters, news reports from the Australian, the Financial Times, Bloomberg and ABC News.

Global stock markets have experienced a wild ride in recent months as the Australian share market reached two year lows in late September on the back of fears of slower world growth led by China. This caused a slide in commodity prices which flowed onto the ASX All Ordinaries Index together with concerns about when the US Federal Reserve will raise interest rates. Market sentiment was also impacted by commodity trader and resources company Glencore which was sold down heavily on worries about its $50bn debt and lower commodity prices while the investigation into Volkswagen’s emissions testing scandal hit the global automotive sector putting further pressure on markets.

China worries increased in August and continued into September following the depreciation of its currency to help stimulate its economy and boost exports. Poor recent data releases added to the negative market sentiment with Chinese industrial profits declining by 8.8% in August compared to the previous month and its biggest fall on record. Manufacturing data measured by the Caixin Purchasing Managers’ Index (PMI) came in at 47.2 for September, below forecasts of 47.5 to reach its weakest level since April 2008 indicating slower growth for China. The official manufacturing PMI was 49.8 for September, slightly above the 3 year low of 49.7 reached in August where a reading above 50 indicates expansion in factory activity compared to contraction at levels below 50. The official PMI is based on the larger Chinese state enterprises while the Caixin sponsored PMI focuses on a small sample of private companies to provide a measure of manufacturing activity.

The US Federal Reserve (Fed) left interest rates on hold in September with Fed Chair Janet Yellen citing the uncertainty in China, subdued US inflation and a rise in the value of the US dollar was tightening financial market conditions impacting the global economic outlook. The Fed stated that “Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term…The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring developments abroad.” Yellen followed up the Fed statement with comments that the US economy is strengthening and a rate increase is likely later this year. This was backed up by the US 2nd quarter GDP growth being revised upwards to 3.9% from the initial estimate of 3.7% and 0.6% growth in the first quarter. Disappointing jobs data for September provided less reason for the Fed to hike rates any time soon with the US economy creating only 142,000 jobs for the month, well below expectations of 203,000 new jobs as the unemployment rate held steady at 5.1%.

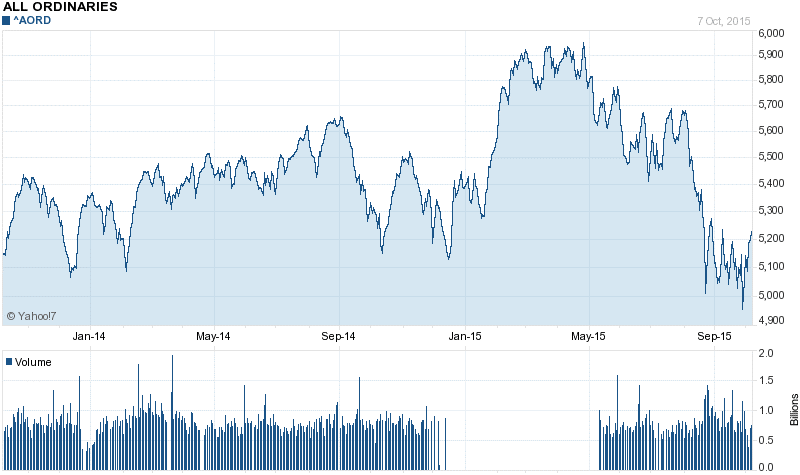

With Australia portrayed as a “China and commodities play”, the Australian share market as measured by the All Ordinaries Index fell below the 5,000 level in late September. This was due to the negative global news which caused the All Ord’s to reach a two year low as seen by the chart below sourced from Yahoo!7Finance:

On a Price to Earnings basis, the Australian share market reached a relative cheap PE level of around 11.5 times earnings during the September sell off with a corresponding market dividend yield of 7%. The All Ord’s has subsequently bounced in early October to now be pushing 5,300 and is up about 6.5% from its lows. BHP hit a 7 year low of $21.61 and PE of 12 times as resource stocks were heavily sold down in a market over reaction to China. The BHP and RIO CEOs commented that export volumes to China have not declined and that China’s inventory levels have not increased. BHP has since rebounded in line with higher oil and commodity prices to now be trading over $25.

Current PE levels and dividend yields on some of the Australian market’s popular stocks are as follows:

|

ASX Code – Company Name |

PE Ratio |

Dividend Yield (ex Franking) |

|

BHP – BHP Billiton |

16.3 |

6.9% |

|

HVN – Harvey Norman |

15.7 |

5.2% |

|

CBA – Commonwealth Bank |

13.9 |

5.6% |

|

ANZ – ANZ Bank |

10.6 |

6.5% |

|

NAB – National Aust. Bank |

12.8 |

6.3% |

|

WBC – Westpac Banking Corp. |

12.5 |

6.0% |

|

All Ordinaries Index |

15.6 |

4.6% |

Sources: Commsec, Morningstar

Outlook

Global growth forecasts from the International Monetary Fund (IMF) have been downgraded from previous estimates of 3.3% to 3.1% forecast growth for 2015. The growth estimate for 2016 has also been cut by 0.2% to 3.6% due to a slowdown in emerging markets driven by weak commodity prices. China’s growth is forecast to be 6.8% this year and 6.3% for next year while Australia’s economy is expected to grow 2.4% in 2015 and 2.9% in 2016, below the Reserve Bank of Australia’s trend growth target of 3%. This leaves the door open for the RBA to cut rates further to support the economy and drive the AUD lower following its decision this week to leave the official cash rate steady at 2% for the fifth straight month. The direction of markets in the short term will be led by the US 3rd quarter company reporting season which kicks off this week with expectations of bumpy earnings due to the strong USD and a lack of guidance to result in company surprises. However, with the Australian banks (with the exception of the CBA) heading into their reporting and ex-dividend period, this has normally been a time of solid returns as the banks rally ahead of going ex-dividend. This will provide a good lead-up to the traditional rally into Christmas especially with forecasts of a US rate rise being pushed back to March 2016 being supportive of markets.

You can download the market index returns from Morningstar below for the various asset classes to the end of September 2015.

This article is intended to provide general information only, and is not to be regarded as legal or financial advice. The content is based on current facts, circumstances, and assumptions, and its accuracy may be affected by changes in laws, regulations, or market conditions. Accordingly, neither Azure Group Pty Ltd nor any member or employee of Azure Group or associated entities, undertakes responsibility arising in any way whatsoever to any persons in respect of this alert or any error or omissions herein, arising through negligence or otherwise howsoever caused. Readers are advised to consult with qualified professionals for advice specific to their situation before taking any action.

Comment