Part 1-Structuring insurance in a tax effective way inside super

- Do you and your family have adequate insurance cover?

- When was the last time you reviewed your insurance to your actual needs today?

- Is there a more tax-effective way to fund insurance premiums inside super?

- What is the down side?

How does this work?

Personal insurance is an effective way to provide an instant asset that protects your quality of life, provides support for your loved ones if you die, or can’t work if you get sick, injured or suffer a major traumatic event.

While you often hear how important it is to have sufficient cover, it’s just as important to be smart about the structure of your insurance – so the premiums work harder for you.

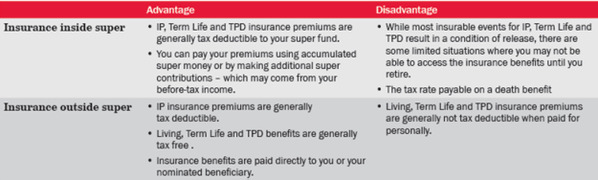

Most types of life insurance can be held inside or outside of super. These include:

• Income Protection (IP) - Pays a regular monthly benefit if you become severely disabled by sickness or injuries and you are unable to work – potentially helping you cover mortgage repayments and provide a significant but reduced income to live on

• Crisis/Trauma Insurance - Pays a tax free lump sum if you suffer a serious illness like cancer, a stroke or heart attack and assists covering major medical expenses, home modifications and/or paying for help around the house, possibly the mortgage and a supplement to Income Protection insurance

• Term Life Insurance - Pays a lump sum benefit if you die or become terminally ill – helping your family take care of debts and ongoing household expenses.

• Total & Permanent Disablement (TPD) Insurance - Pays a benefit if you are permanently disabled – helping cover the long-term costs of care for you and your family.

Here is a summary of the advantages and disadvantages of having insurance inside or outside super.

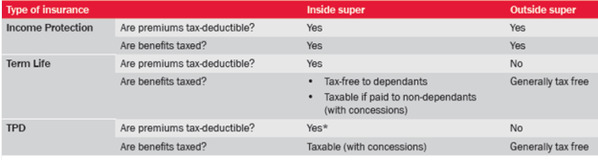

Tax treatment at a glance

Below is a table summarising the tax treatment of premiums and payment inside and outside super.

*Tax deductions for own occupation may only be partially deductible - this can be a big deal.

What does this mean for me?

The decision to have insurance cover inside super depends on your personal circumstances, estate planning strategy, stage of life and needs. By choosing the right combination, you have the appropriate insurance cover to give peace of mind, meet your goals and objectives and for premiums to be tax-effective

How structuring insurance via super is tax-effective

As the table below shows, the higher your personal marginal tax rate, (the rate you pay tax) the bigger the potential saving by having insurance inside super.

Before-tax cost of a $1,000 insurance premium:

Source: BT Life Insurance. Assumes insurance is arranged through a taxed super fund.

Note: Most insurance premiums are tax deductible to super funds so it may offset other taxable income (such as concessional super contributions).

What is the down side?

The trade off includes:

- The premiums reduces your balance in the fund that could have been accumulated for your retirement

- Some super fund trust deeds may not be able to pay insurance proceeds to you until a condition of release is triggered

- The definition of Total and Permanent Disablement may be restrictive compared to the any occupation definition available outside super

- Crisis/Trauma insurance inside super is problematic

Please tune in for Part 2 - When to have insurance outside super in our June Newsletter.

For more information, please contact Azure Group Wealth at ourteam@azuregroup.com.au or (02) 9238 1188.

This article is intended to provide general information only, and is not to be regarded as legal or financial advice. The content is based on current facts, circumstances, and assumptions, and its accuracy may be affected by changes in laws, regulations, or market conditions. Accordingly, neither Azure Group Pty Ltd nor any member or employee of Azure Group or associated entities, undertakes responsibility arising in any way whatsoever to any persons in respect of this alert or any error or omissions herein, arising through negligence or otherwise howsoever caused. Readers are advised to consult with qualified professionals for advice specific to their situation before taking any action.

Comment