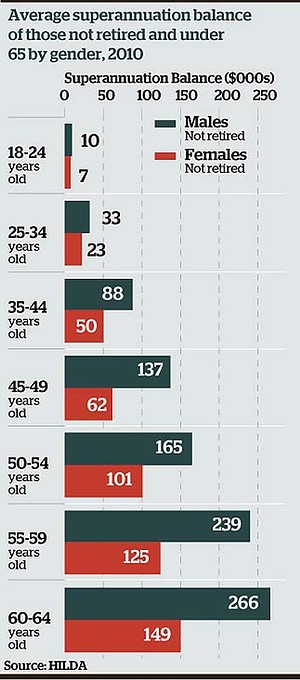

When women are in their 30s and 40s trying to navigate the delicate balance of continuing their careers and taking care of a family, planning for their retirement often ends up quite low on their priority list. Unfortunately, it’s not something a lot of women play close attention to as it doesn’t appear to be an immediate concern. It is no secret that the super industry is trying to improve their engagement with women. In 2012 theAssociation of Superannuation Funds of Australia (ASFA) along with Suncorp conducted a survey and found that women were more likely than men to feel ''inadequate, ashamed or dumb'' when it came to their superannuation. Furthermore, 40% of the women surveyed said they felt “powerless”.

With a number of hurdles in the way, it is quite critical for women to think ahead. Things like the longer average life span, halted earnings due to time taken out to have children and the still concerning gap between male and female salaries, are all very real hurdles that women need to overcome to ensure their security when it comes to the retirement phase of their lives.

Research by ASFA suggests a 32-year-old woman on $65,000 a year will miss out on $28,000 in super if she takes two years off work; the same woman earning $85,000 a year will be $36,500 behind.

Here are some very practical tips to consider right now, to avoid a shock when it comes to retiring age (Source: The Sydney Morning Herald).

- If you're planning to have children at some point, boost your super contribution now. You'll benefit from the compound interest on those contributions for the rest of your life.

- Go to the MoneySmart website to work out how much extra contributions could add to your super balance. A 40-year-old earning $50,000 with a balance of $35,000 - the median for women aged 35-44 - could boost her $259,827 balance at age 67 by more than $8000 by salary-sacrificing just $20 a month.

- If you're on a low- or middle-income wage, check whether you're eligible for the government's co-contribution scheme. This gives a tax-free boost of up to $500 for workers on less than $46,920 who contribute extra to their super.

- If you're on maternity leave or working part time, consider whether your partner could contribute to your super.

- If you're back at work after taking leave, consider boosting your super contributions now. ASFA and Suncorp suggest following the ''1 per cent rule'' - contribute an extra 1 per cent to your super for every two years spent out of the workforce.

- If you're thinking about changing jobs, assess the super and parental leave policies of potential employers.

For more information, please contact Azure Group Wealth at ourteam@azuregroup.com.au or (02) 9238 1188.

This article is intended to provide general information only, and is not to be regarded as legal or financial advice. The content is based on current facts, circumstances, and assumptions, and its accuracy may be affected by changes in laws, regulations, or market conditions. Accordingly, neither Azure Group Pty Ltd nor any member or employee of Azure Group or associated entities, undertakes responsibility arising in any way whatsoever to any persons in respect of this alert or any error or omissions herein, arising through negligence or otherwise howsoever caused. Readers are advised to consult with qualified professionals for advice specific to their situation before taking any action.

Comment