In our last blog we made it clear that companies performing eligible R&D activities must think scientifically – that their R&D must proceed from hypothesis to experiment, observation and evaluation, and lead to logical conclusions.

The very beginning of this systematic progression of work is the planning stage, and it is the focus of this week’s blog. We will discuss the myth that a company undergoing normal product testing or quality assurance can consider this eligible for R&D incentives – even if it leads to new knowledge that would otherwise be eligible.

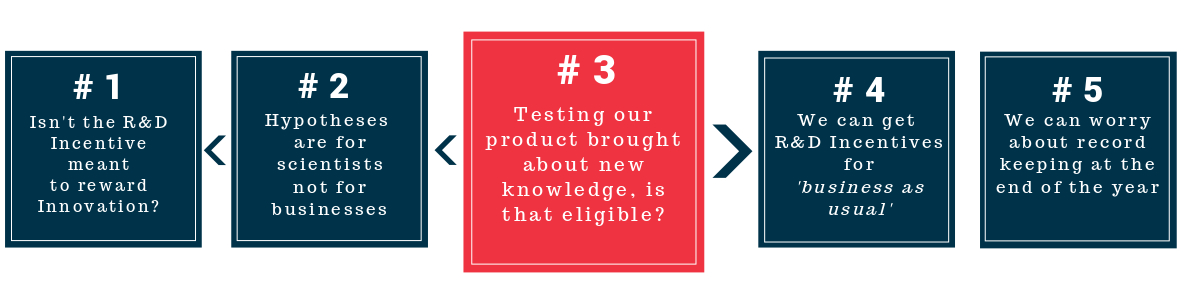

#3 TO BE ELIGIBLE FOR R&D, THE SIGNIFICANT PURPOSE OF EXPERIMENTAL ACTIVITIES MUST BE TO DEVELOP NEW KNOWLEDGE

At the inception of any experimental activity, there may be a number of different reasons for undertaking these activities. However to be eligible for R&D, the significant purpose of those activities must be to develop new knowledge. The concept of significant purpose can be illustrated in the example below:

“An agriculture company is experiencing poor growth and poor-quality crops. The company undertook activities across its entire farm to transform it from a conventional farm using chemicals to a more sustainable farm based on a biological input regime.”

To the untrained eye, the company’s outcome from experimental activity would be considered an eligible R&D activity, however in the interpretation of the regulators here the main intention was ultimately not to generate new knowledge, but rather business-driven to improve its efficiency and financial position. Generating new knowledge must not be auxiliary intention or an afterthought, and this must be clear at the outset of experimentation as part of your hypothesis.

A practical application of this concept can be seen in a Tribunal decision for JLSP and Innovation Australia [2016] AATA 23 which held that the company conducted its clinical trials to determine the safety and efficacy of a drug for to fulfil its contractual obligations and for regulatory purposes – and not to generate new knowledge. Innovation Australia took no issue with the nature of the company’s activities meeting the core R&D definition; the contest was purely over the purpose test.

The mere existence of more than one purpose of undertaking activity does not preclude the generation of new knowledge from being a significant purpose. The decision of the Tribunal confirmed this by stating “[…] the purpose of generating new knowledge does not have to be the purpose that outweighs all others, instead consider that the purpose of generating new knowledge must be more than an insubstantial purpose […] even if at the same time other substantial purposes exist.”

SOFTWARE DEVELOPERS: Avoid the pitfall of equating experimental activity with normal testing

In determining the significant purpose of experimental activities, it is also important to avoid the pitfall of equating experimental activity with normal testing. This error is particularly prevalent in the software development industry whereby the testing of software such as bug testing, system testing, data mapping and migration testing is regularly conducted. These activities are fundamentally not considered eligible R&D activities as they are not conducted to test a hypothesis. These tests are normal activities that any software developers can perform successfully using their existing knowledge. We will consider this in more depth next week, as we discuss why you can’t receive R&D incentives for 'business as usual' activities.

Why are we talking about it for the whole month of October?

Well we think it's important to demystify R&D and explain why now more than ever a careful focus on eligibility is key.

Over the month of October, we are exploring 5 misconceptions in a series of blogs, leaving you with a downloadable booklet to keep on hand when you are exploring R&D. We dive deeper into satisfying the different eligibility tests from this legislation using real-world examples to cut though the fog of confusion the market is having on eligible businesses.

|

|

Keep your eyes peeled for Blog #4 and #5 and follow us on socials.

This article is intended to provide general information only, and is not to be regarded as legal or financial advice. The content is based on current facts, circumstances, and assumptions, and its accuracy may be affected by changes in laws, regulations, or market conditions. Accordingly, neither Azure Group Pty Ltd nor any member or employee of Azure Group or associated entities, undertakes responsibility arising in any way whatsoever to any persons in respect of this alert or any error or omissions herein, arising through negligence or otherwise howsoever caused. Readers are advised to consult with qualified professionals for advice specific to their situation before taking any action.

Comment